Doka UK 25 April, 2019.-The Construction Industry Training Board (CITB) uses its research and labour market intelligence to understand the sector’s skills needs, and works with industry and government to ensure that the construction industry has the right skills, now and for the future. In this article, we base our discussion around analyses of the most dominant construction sectors over the coming years with research findings from the CITB and Experian research.

The CITB is modernising its funding approach to invest in areas that will deliver the best returns for the construction industry, thus enabling the sector to attract and train talented people to build a better Britain.

Experian’s Construction Futures team is a leading construction forecasting team in UK, specialising in the economic analysis of the construction and related industries in UK and its regions. The Construction Futures team has collaborated on the Construction Skills Network employment model with the CITB since 2005, managing a monthly survey of contractor’s activity as part of the European Commissions’ harmonised series of business surveys, and a quarterly State-of-Trade survey on behalf of the Federation of Master Builders.

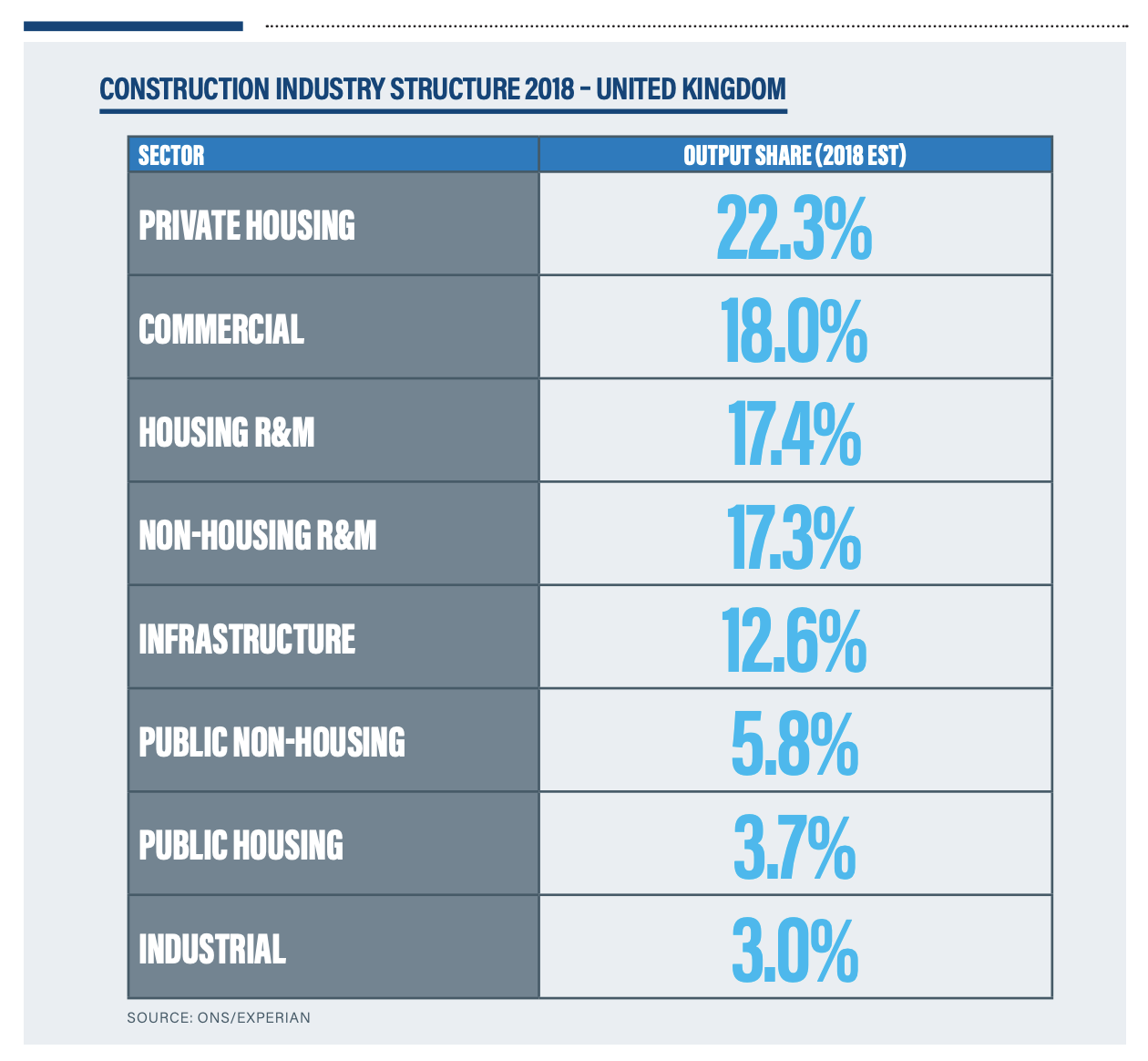

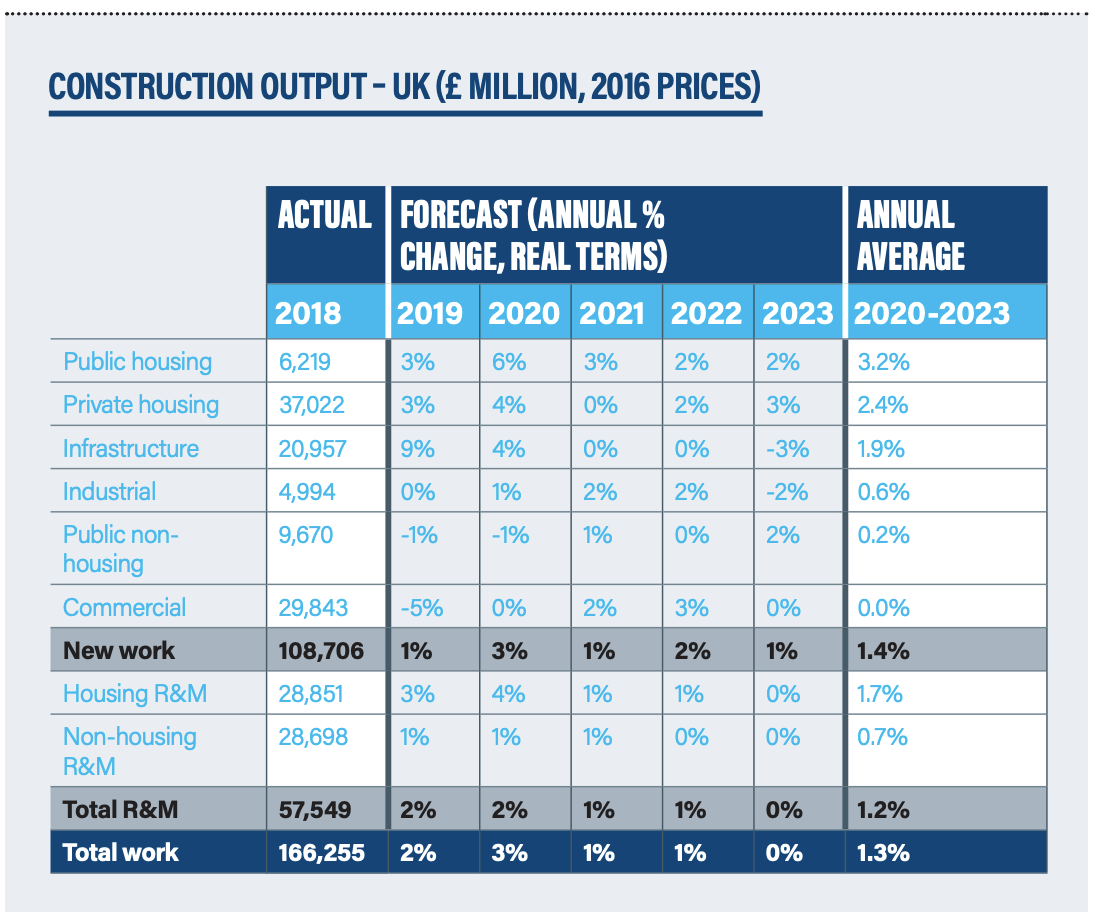

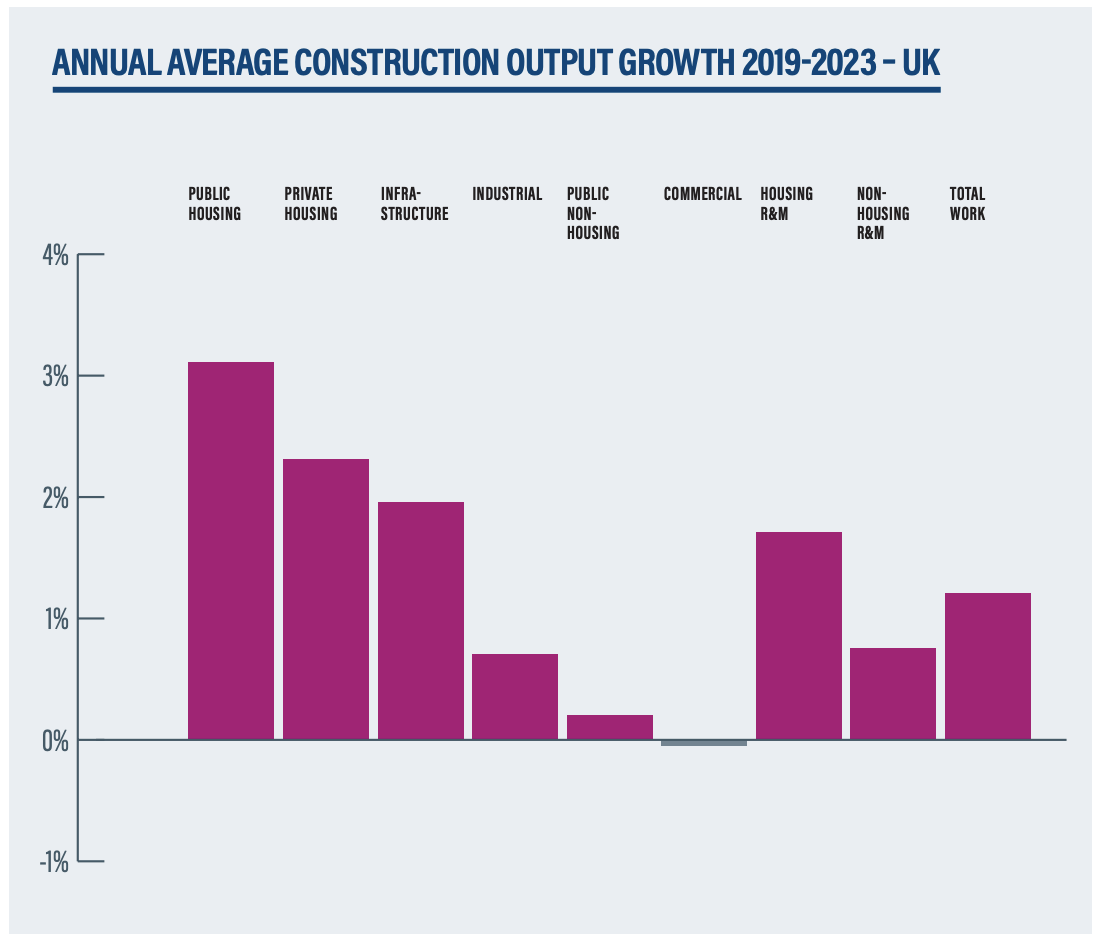

The construction sector can be divided into several sectors. In this instance, with the information from CITB and Experian, we focus on a few of these:

- Infrastructure. Transport and energy projects will be the main drivers of infrastructure output growth from 2019-23. Hinkley Point C’s main works started this year while activity on phase 1 of HS2 has been forecast to increase. Wylfa Newydd, in Wales, has joined Moorside in the North West as nuclear new build projects that have stalled. Further impetus will come when Highways England’s roadbuilding programme gains momentum, although there are concerns that the agency is struggling to keep projects on schedule, not least because of capacity issues. According to the Autumn 2018 update of the Government’s National Infrastructure and Construction Pipeline (NICP), potential total expenditure on infrastructure projects (public and private) is indicated at around £151bn (2017/18 prices) between 2018/19 and 2020/21, with a further £218bn in the pipeline post-2021.

- Education and Health Construction.The non-housing building sectors fared poorly in 2018 (industrial construction excepted) and are expected to continue to underperform relative to the housing and infrastructure sectors. Government focus on housing has meant less emphasis on other areas. Output in the public non-housing sector in 2018 is estimated to have fallen to its lowest level since 2007 in real terms. Anecdotal evidence suggests work under the Priority School Building Programme has not emerged as anticipated, because government has cooled on free schools. The National Construction and Infrastructure Pipeline indicated a falling profile of investment in the public non-residential sector between 2018-19 and 2020-21, with only the health building sector showing a potential increase.

- Industrial.The components of industrial construction are likely to move in different directions as Brexit uncertainties impact on them. The manufacturing sector is expected to be negatively affected by trading uncertainties due to Brexit, while the warehouse sub-sector could benefit from the need for more storage facilities as current ‘just in time’ systems become harder to maintain. The two factors are expected to largely cancel each other out, in forecasting terms, giving only modest growth for the sector as a whole.

- Commercial Construction.The expected decline in commercial construction, as a result of the cautious stance taken by investors in the aftermath of the vote to leave the European Union (EU) , has finally come to pass; output was down an estimated 5% in real terms in 2018. It has taken time for this more cautious stance to feed through into the statistics. The 24% decline in new orders for office construction in 2017 is telling, although they did pick up a little last year.

- Retail Construction.Retail construction remains in the doldrums and the strong growth seen recently in the leisure sub-sector has ended. The prognosis for the commercial sector as a whole remains poor for the next couple of years, with output only starting to grow again in 2021.

Employment within the construction sector

Employment is projected to rise over the 2019 to 2023 period at an annual average rate of 0.5%, in line with the whole economy average. UK construction employment is expected to reach 2.79 million in 2023, just 2% lower than the 2008 peak as stated in the Construction Skills Network report published by CITB and Experian:

- Demand: Annual Recruitment Requirement.The average annual recruitment requirement (ARR) is estimated at 33,700 for 2019-23, slightly higher than that predicted for the 2018-22 period (31,600). Since employment growth returned in 2014, it has been stronger among the managerial/admin and professional occupations and, weaker among the trades/elementary ones, although most of the 28 occupational categories have seen some increase. This trend is expected to continue from 2019-23.

- Professions in High Demand.The 33,700 ARR means industry will need to recruit an extra 168,500 workers over the next five years. In absolute terms, the highest ARRs for construction roles are for construction process managers (3,420), other construction professional & technical staff (3,260), and wood trades & interior fit-out (2,380). As a proportion of base 2019 employment, the biggest requirements are predicted for scaffolders (3.1%), logistics personnel (2.6%), and plant operatives (2.3%).

Documentation in: CITB Research