UK, April 18, 2018.-The growth of the construction sector in the UK lost its pace at the end of 2017 due to a number of factors such as the uncertainty of the post-Brexit deal, increases in inflation and a reduction in economic growth. The unexpected weather conditions (Beast from the East) during March could also be argued to be a contributing factor. For this reason, at Doka UK we have decided to analyse a snapshot of the construction industry with several business organisations and a group of experts. Our professional information sources include the following:

1.- Infrastructure Intelligence (produced for the industry by the Association for Consultancy and Engineering). This digital magazine has published precise and rigorous details about the latest news that have been registered by the UK construction sector.

2.- Richard Robinson is the chief operating officer at AECOM and proposes real innovation models applicable from day to day.

3.- Ramboll UK Managing Director Mathew Rileycalls for a digital revolution and encourages making the right decisions in a hopeful exercise.

4.- Atradius market monitor focuses on Construction Sector Performance, outlook and a specific analysis of the UK construction sector.

According to the publication of the digital magazine, Infrastructure Intelligence, in several news articles, the “unusually bad weather” which was brought by the ‘Beast from the East’ last month was one of the factors which led to total construction output falling at the fastest pace since July 2016, according to the latest IHS Markit/CIPS UK construction purchasing managers’ index (PMI). Results show that growth plummeted from a score of 51.4 in February to 47 in March, meaning it is the first time construction activity fell below the 50 no-change marker for six months. A reading above 50 indicates growth, and below 50 a contraction. According to Markit, the snow disruption had a “particularly negative” impact on civil engineering projects, which witnessed the sharpest activity fall since 2013.

The snow and ice which fell uncharacteristically in March meant survey respondents said that the bad weather had been a disruption to staff availability and activity on site. Despite the poor figures, Tim Moore, Associate Director at IHS Markit, believes there is some room for optimism with a rise in employment figures and the positive stance on business activity expectations in nine months.

Commenting on the figures, Moore said: “The construction sector continued to experience subdued business conditions during March”, Moore continued “total construction output fell at the fastest pace since July 2016, driven by the sharpest reduction in civil engineering activity for five years and a renewed fall in commercial work.

Mark Robinson, Scape Group Chief Executive believes today’s PMI shows how the impact of the weather “demonstrates the fragility of the construction sector”. He said: “While we cannot control mother nature, we should at least be in a position to ensure that there is a solid line of current and future work in place and that contingency plans are available to deal with meteorological events that could become more frequent occurrences in our changing climate”.

Richard Robinson – Chief Operating Officer at AECOM

Richard Robinson, Chief Operating Officer at AECOM has recently published some interesting reflections. He reports it is no secret that the delivery of critical infrastructure assets is crucial to a country’s economic growth and the wellbeing of communities. Yet around the world, infrastructure issues such as highway congestion and unreliable rail networks continue to persist.

The 500 industry professionals surveyed in AECOM’s recently published Future of Infrastructure report say they have suffered significant yet avoidable delays on 40% of recent projects. This could be a thing of the past if a combination of technology and alternative delivery is adopted, both key to tackling the productivity issue and accelerating much-needed projects.

Currently, many infrastructure projects are slowed down due to inefficient and outdated project delivery methods that lead to delays and schemes that run over time and budget. The effect on the UK economy is damaging, with the cumulative impact of stalled projects during 2015-16 alone projected to dent investment-related GDP to the tune of £35bn.

There are many reasons why there’s often a drag on productivity. A fragmented supply chain with sub-optimal integration across different services is among the top concerns, as well as limited consideration of total cost of ownership or total life-cycle implications. Resistance to change with the project cycle is another issue, along with the effect of low margins on research and development investment. One issue is found in the recent Future of Infrastructure report was limited adoption of new technology and best practices. Worryingly, the report found that only 56% of industry professionals consider themselves “good” at adopting and scaling innovative delivery models.

This all results in a domino effect where buyers get inefficiency, often resulting in delayed projects and poor-quality assets, and suppliers struggle to survive financially. This is despite the fact that there are several tools and approaches available to produce a positive transformation in the delivery of major infrastructure projects. The challenge is to effectively learn lessons from the past, to build a new industry dynamic.

A two-step approach to solving the productivity issue is needed, which firstly sets up projects differently to incorporate a more integrated approach, linking across the life cycle of an asset and reducing total cost of ownership. This would also create assets that are more constructible and fit for purpose. Secondly, using digital tools to unlock the full power of this integrated approach is essential.

To achieve the first objective, breaking down the familiar approach of plan, design, build, operate and maintain will be key. Infrastructure organisations should seek to align all objectives and rewards across the supply chain to meet the client’s key success factors. A more honest dialogue around risk is needed, with suppliers providing greater transparency around the true nature of risk in their schemes and infrastructure owners willing to take on risks they are better positioned to manage themselves.

Well-designed and performance-based partnership models that are incentivised to deliver the best for the project and client are crucial. Ultimately, it’s about getting the basics right – robust project setup; streamlined governance; and continuous stakeholder buy-in.

Next in the two-pronged approach is the use of digital tools. These can bring efficiencies in each individual service line as well as enable the full power of an integrated approach. Enhanced and automated value engineering to create a more buildable and operable asset is just one example.

For example, virtual reality (VR) solutions have the potential to merge separate delivery phases by offering an interactive and easily accessible digital design model. AECOM has used this technique on projects as diverse as the Wessex Capacity project at Waterloo and the Serpentine Pavilion in Hyde Park, enabling them to deliver schemes more efficiently than ever before. This technology enabled stakeholders to walk through a design in the virtual environment and provide immediate feedback. Other benefits include the ability to remove safety hazards, optimise build sequence and schedule and minimise the need for re-work.

Other digital tools that are growing in impact include artificial intelligence that replaces repetitive manual tasks and provides a more reliable outcome. This enables new construction techniques such as the use of modular construction, 3D printing, the increased use of robotics. Asset and build intelligence is also on the up, for example the remote measuring of temperature and strength development of in-situ concrete maturity with systems such as Concremote.

Capturing operational data is nothing new, but the volume of data and the ability to effectively analyse and draw conclusions is taking a step change when AI and other data mining techniques are coupled with today’s computing power. This allows new tools to capture and analyse performance data to drive more efficient operations and truly feed back into future designs.

After years of industry wrestling with the productivity gap, the time has come to fully embrace innovation and take the necessary step forwards to accelerate delivery. We now have the keys to unlock the future – and they lie in the combination of new delivery models and the smart use of technology.

Ramboll UK Managing Director Mathew Riley calls for a digital revolution

As explained by Mathew Riley: An increasing number of organisations are developing their own offsite supply chain, to help tackle this crisis when called upon. This is encouraging, but only part of the story. By combining digital design with offsite construction, the industry can feasibly deliver design, engineering and construction the way it should be. Riley believes that embracing such techniques could boost overall productivity in the sector by up to 40%.

However technological advancement without practical experience can create solutions that don’t deliver or integrate. We need both the government and industry leaders to wake up to the potential transformative benefits of innovation and help deliver a standardisation of digital tools and methods.

However, realising the benefits of these developments will become easier the more they are adopted. Massive time compression will result (and time is money), along with safer design and delivery, productivity and improved sustainability. The construction industry will reap rewards, such as a new set of skills to offset the perceived skills shortage, dramatically reduced onsite labour costs, and most of all a sustainable business model that competes alongside other industries for the best talent. Complex problems can be solved with dynamism and innovation, to deliver iconic projects and contribute to the wider built environment.

So, in light of the recent economic contraction, this is good news for the industry and economy. If embraced, such an approach will transform productivity across our industry, saving potentially hundreds of millions of pounds. This is design, engineering and construction the way it should be – and the revolution could be about to begin.

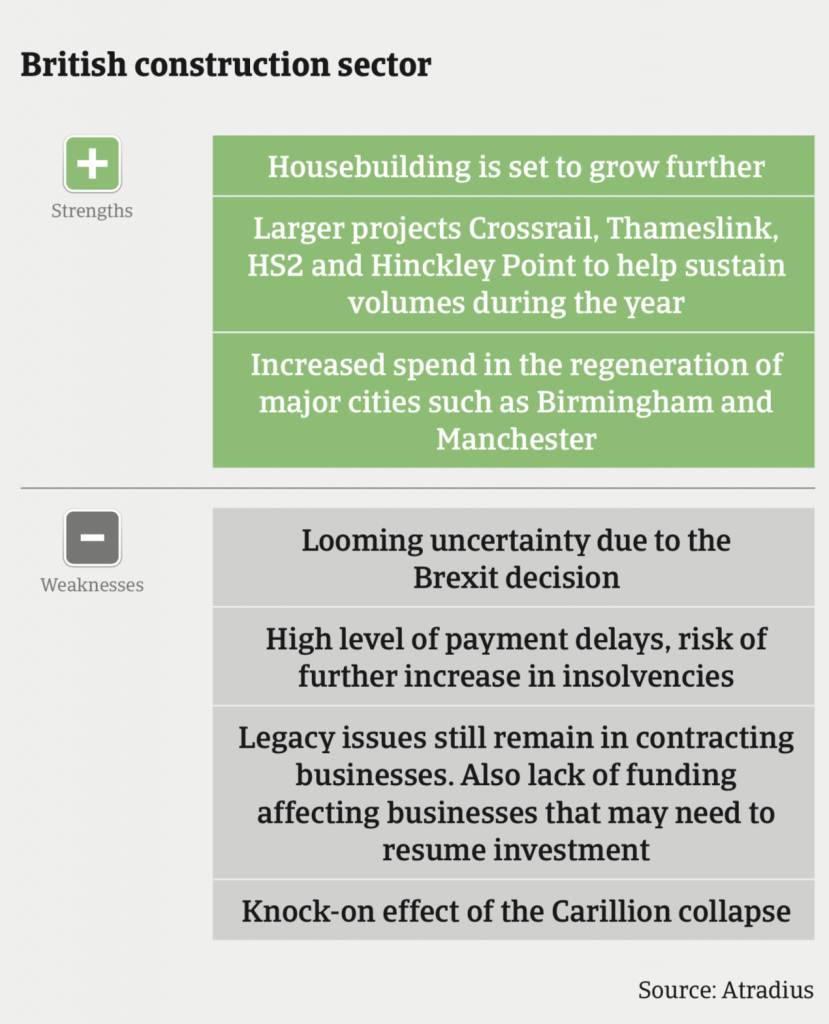

Atradius Market Monitor: Focus on Construction Sector Performance and Outlook February 2018

Legacy contracts have been a serious issue for the construction industry over the past 3-4 years, as many businesses pursued an aggressive accounting strategy by sealed risky contracts which proved unprofitable. Problems have been exacerbated by rising raw materials and labour costs. In 2017 four out of the top 10 construction companies in the UK issued profit warnings, and in January 2018 Carillion, the 2nd largest construction company in the UK and one of the government’s biggest contractors, filed for voluntary liquidation, struggling under GBP 1.5 billion of debt including a pension shortfall of GBP 587 million.

The subsequent knock-on effect is expected to be huge, as it is anticipated that between 25,000 and 30,000 suppliers and sub- contractors are owed around GBP 2 billion. This will surely cause substantial financial distress for thousands of suppliers along the value chain.

Average payment in the British construction industry is 75 days, and the level of protracted payments and payment delays remains high. After increasing in 2017, the level of non-payment notifications is expected to increase further in H1 of 2018, additionally fuelled by the Carillion liquidation. For many smaller construction businesses problems further up the supply chain regarding delays in payments will only intensify the issues they already have and drain them of their “lifeblood” of cash, which could have serious repercussions on their performance. With the problems experienced by tier one contractors in 2017 and the Carillion liquidation, access to bank finance remains difficult, especially for smaller construction businesses and companies in sectors such as support services, particularly those with feeble balance sheets.

Due to all this and a general concern over the overall state of the UK economy, the level of insolvencies in the construction sector will remain high and is expected to increase further in 2018, by about 4%-5% year-on-year.

Beside the current market shake-up caused by the Carillion liquidation, the Brexit issue will undoubtedly have an impact on the construction market, as the industry is very susceptible to shifts in investor confidence. If the coming months fail to deliver greater clarity about the conditions under which the UK will leave the EU, the commercial and infrastructure segments in particular could struggle.

As more than 60% of building materials are imported from the EU, any increase in tariffs or limits on quantities imported after leaving the EU could lead to higher costs for British construction businesses and a shortage of building materials. Once the UK leaves the Single Market it is likely that the current issue of skill shortages will worsen, especially if there are no follow-up agreements with the EU on the free movement of people. This could result in even higher pressure on wages, causing construction firms to face considerably higher project costs.